Casino vs Sports Preference Stats: Comparing Player Behaviour Across Gambling Segments

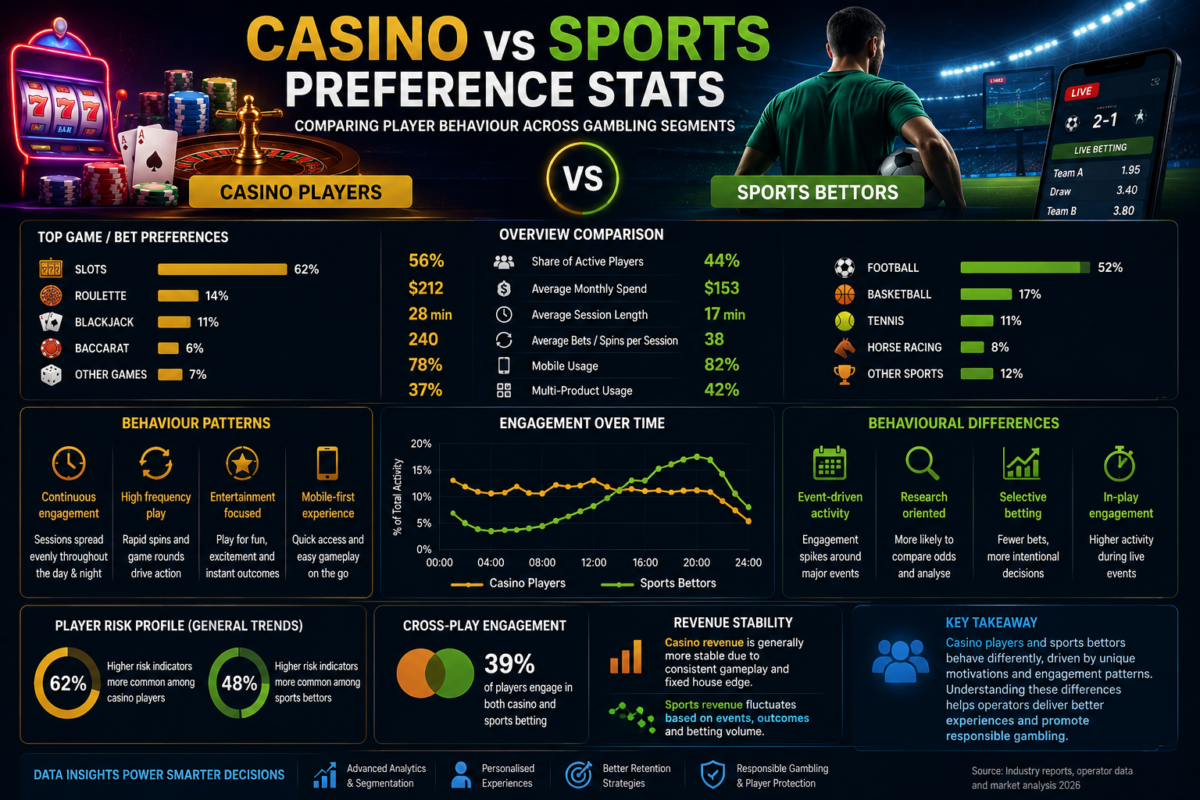

Online gambling markets are increasingly shaped by behavioural differences between casino players and sports bettors. Although both groups operate within the same digital ecosystem, their engagement patterns, risk behaviour and spending structures often differ significantly.

This report examines the key behavioural and structural differences between casino-focused users and sports betting audiences across regulated online gambling markets.

Sports Betting and Casino Gambling Attract Different User Profiles

Casino players and sports bettors often demonstrate fundamentally different motivations and engagement styles.

Sports bettors typically engage with:

- match analysis

- team loyalty

- event-based excitement

- statistics and predictions

- competitive sports culture

Casino users, by contrast, are more commonly driven by:

- continuous gameplay

- entertainment pacing

- instant outcome cycles

- visual stimulation

- rapid session engagement

These differences strongly influence behavioural patterns and platform usage.

Sports Bettors Tend to Follow Event-Based Behaviour

Sports betting activity is heavily connected to sporting calendars and live events.

Peak engagement periods often include:

- football weekends

- major tournaments

- playoff seasons

- horse racing festivals

- international competitions

This creates cyclical betting behaviour linked to external sporting schedules.

Sports bettors are generally more likely to:

- research events beforehand

- compare odds

- follow specific teams or leagues

- place fewer but more intentional wagers

Engagement intensity often fluctuates depending on sporting activity.

Casino Players Display More Continuous Engagement

Casino behaviour patterns are typically less dependent on external events.

Online casino players frequently demonstrate:

- longer session duration

- continuous gameplay cycles

- faster wagering frequency

- increased repetition behaviour

- higher overnight activity

Because casino games operate continuously, engagement becomes less seasonal and more habit-driven.

This creates fundamentally different retention and monetisation dynamics compared to sports betting.

Mobile Usage Is Strong Across Both Segments

Both casino players and sports bettors now operate primarily through mobile platforms.

However, behavioural differences still exist.

Sports betting mobile activity often centres around:

- live events

- in-play betting

- score tracking

- notifications and odds movement

Casino mobile engagement is more associated with:

- rapid accessibility

- convenience-driven sessions

- short repetitive gameplay cycles

- instant interaction patterns

Mobile-first behaviour has accelerated growth across both verticals.

Betting Frequency Differs Significantly

Sports bettors generally place fewer wagers compared to casino users.

Typical sports bettor behaviour includes:

- event-focused sessions

- selective market participation

- lower spin frequency equivalent

- longer decision cycles

Casino players, meanwhile, often generate:

- significantly higher action volume

- shorter gameplay intervals

- continuous wagering sequences

- repeated rapid interactions

This creates different exposure and volatility profiles between the two segments.

Risk Profiles Often Vary Between Segments

Behavioural risk characteristics differ notably between sports and casino audiences.

Casino-focused users often display:

- higher continuous engagement

- elevated session duration

- stronger repetitive behaviour patterns

- faster wagering cycles

Sports bettors are more likely to demonstrate:

- emotionally driven event wagering

- loyalty-based decision making

- outcome attachment to favourite teams

- live event impulsivity

Both segments contain unique behavioural risk indicators requiring different responsible gambling approaches.

Operator Revenue Structures Differ

Casino and sportsbook operators rely on different monetisation mechanics.

Sports betting revenue is influenced by:

- bookmaker margins

- market volatility

- event outcomes

- betting volume fluctuations

Casino revenue is generally more stable due to:

- mathematically fixed RTP structures

- continuous gameplay

- predictable long-term house edge

This often makes casino products more operationally stable from a revenue perspective.

Cross-Sell Between Sports and Casino Continues Growing

Modern gambling platforms increasingly encourage crossover engagement between verticals.

Common cross-sell strategies include:

- sportsbook-to-casino migration

- casino lobby integration within betting apps

- unified wallets

- shared loyalty systems

- event-triggered casino promotions

Operators aim to maximise lifetime user value by increasing multi-product engagement.

Behavioural Analytics Shape Both Segments

Modern gambling platforms heavily rely on behavioural analytics systems to monitor engagement patterns.

Analytical models examine:

- session length

- wagering frequency

- deposit behaviour

- product preference

- volatility exposure

- retention probabilities

Data-driven segmentation now plays a central role across both casino and sportsbook ecosystems.

Future Trends in Gambling Preference Behaviour

The distinction between sportsbook and casino ecosystems is expected to become increasingly blurred.

Future developments may include:

- hybrid gambling interfaces

- AI-driven personalisation

- integrated entertainment ecosystems

- cross-product engagement modelling

- predictive behavioural targeting

Operators continue evolving toward fully personalised multi-vertical gambling platforms.

Conclusion

Casino players and sports bettors display significantly different behavioural patterns, engagement styles and risk profiles.

Sports betting remains strongly event-driven and emotionally connected to competition, while casino gambling operates through continuous engagement and repetitive gameplay cycles.

Understanding these behavioural differences is increasingly important for operators, analysts and responsible gambling frameworks as online gambling markets continue evolving.